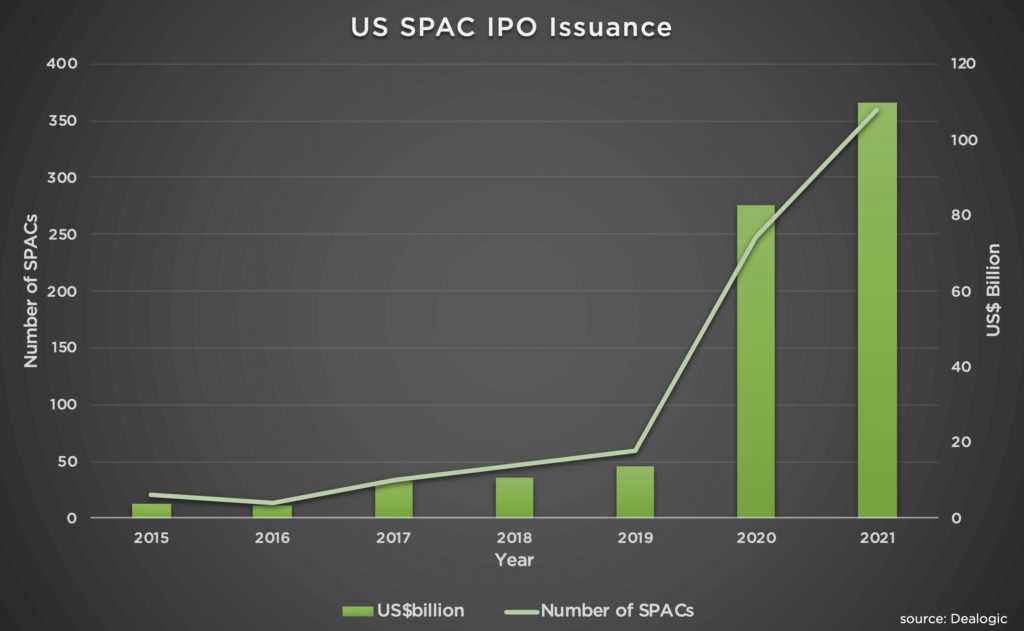

After spending years as something of a sideshow, SPACs took market center stage in 2020, driven by government stimulus programs and expansionary monetary policy. According to data provider Dealogic, in Q1 2021 alone, almost 300 SPACs listed, raising over US$83 billion (see table below). However, since new SEC Chair Gary Gensler introduced tougher oversight of SPACs* and the threat of inflation began spooking the market, SPAC issuances have trailed off significantly: just 13 SPACs listed in April, 19 in May, and 30 in June. Far from that being the end of the story, however, focus is swiftly shifting to the so-called “de-SPAC” phase and the flood of acquisitions soon to follow.

Dealogic data shows that more than 150 SPACs announced acquisitions in the first half of 2021. Nonetheless, over 400 SPACs are still looking for acquisition targets, with many unlikely to ever find a suitable partner to merge with. While sponsors search for deals, prices for suitable candidates are rising. Moral hazard lurks within the SPAC structure and could create serious issues in the near future. Though there is plenty of risk involved in a SPAC, sponsors and advisors can mitigate it by conducting investigative due diligence on every stage of a SPAC’s life cycle.

Refresher: What are SPACs?

A special purpose acquisition company (“SPAC”) is a shell company formed by several sponsors – usually including well-known investors or asset managers – to list on a public exchange and use the capital it raised to identify and acquire a private, operating company. This has the effect of taking the private company public, much like a reverse merger.

The funds raised from the SPAC’s initial listing are held in trust pending a successful merger. The SPAC’s sponsors typically have up to two years to complete an acquisition – or to “de-SPAC” – after the listing. If they fail to meet the predetermined deadline, they must return the initial investors’ money with interest, and the sponsors lose their initial set-up costs as well as their incentives. As a result, there is a strong incentive to find an acquisition target and close a deal.

SPACs are not without controversy. Though a SPAC is often touted as a faster way for a private company to list, the aggregate costs of doing so can be considerable, although not immediately obvious. Initial SPAC investors, often hedge funds, receive essentially free warrants (or private placement warrants) along with their shares. These investors may opt to redeem their shares at the time a deal is cut, receiving their initial funds plus interest, while still holding on to the warrants to purchase additional shares at a predetermined price at a later date. Sponsors are also entitled to a generous slice of shares, called the promote, contingent on a successful deal. Underwriting fees on the capital raised are significant. All of these factors cause dilution and can affect the SPAC’s public investors and the shareholders of the potential acquisition target.

Doing Due Diligence Right – From SPAC…

Investors buy into SPACs because they believe that the sponsors will find them a good deal and make money. Until a deal is announced, there is little more to a SPAC than the credentials of its sponsors and the cash it raises in its listing. This makes it critical to do thorough due diligence on the SPAC’s sponsors, management team, and advisors. In addition to examining their career and professional network, it is important to understand the individuals’ track records and political exposure, as well as ensure that they have not been involved in cases of misconduct.

For a SPAC with an international team, it is imperative to conduct checks not just in the jurisdictions the individuals are currently based but also their prior places of residence. We have seen instances in which individuals have creditors or fraud investigators after them in other countries, but the issues were only disclosed in local legal databases. These potentially deal-killing risks would have been kept under the surface if the checks were only conducted where the individuals were based at the time of the SPAC.

A SPAC sponsor may be a business executive, a private equity fund, or even a company. No matter who or what they are, a key question to ask is, “What are their sources of funds?” Proper due diligence can reveal allegations of fraud within a company, or details like an individual’s career trajectory or close relatives, which may be cause for concern over the sponsor’s source of funding.

For example, one SPAC sponsor was found to be implicated in a wire fraud conspiracy after the SPAC went public. While no charges have been filed against him, his business associate pleaded guilty to charges including money laundering. The sponsor has since been removed from the SPAC.

…To De-SPAC

With more than 400 SPACs looking to de-SPAC within the next year or two, sponsors anxious to close a deal and earn their promote may cast their nets far wider than they should. Startups that had not planned for an IPO so soon and are ill-prepared to do so may be targeted by multiple SPACs looking to take them public. Given the probable hasty decision-making involved in this process, comprehensive due diligence on any acquisition target is essential for the underwriters to get ahead of legal, financial, and reputational risks.

This will involve thorough research on the target’s main operating entity as well as diligence on its executives and directors. Depending on the jurisdictions in which the target is based, an appropriate scope will likely include additional key operating subsidiaries or third parties. In jurisdictions where available public records are limited, the scope should also include conducting discreet source inquiries to gather additional context on existing risk issues.

Example of a De-SPAC Gone Wrong

On 9 September 2019, Modern Media Acquisition Corp. (“MMAC”), a SPAC, merged with Akazoo, a music streaming platform, right before MMAC’s deadline of 17 September 2019.

By May 2020, an internal investigation by a special committee of independent directors had determined that Akazoo’s management team had materially mispresented Akazoo’s business, operations, and financial results, and defrauded Akazoo’s investors, including the MMAC management team. Akazoo’s management team was found to have falsified Akazoo’s books and records, including the due diligence materials the company had provided to MMAC ahead of their 2019 merger. Specifically, Akazoo was found to have inflated its revenue and subscription numbers.

Nasdaq delisted the stock on 27 May 2020, and several securities class action lawsuits against Akazoo and its principals, as well as Lew Dickey, the CEO of the SPAC, remain ongoing.

It Pays to Protect

The critical point to remember is the importance of evaluating both the target company and the SPAC to identify any potential conflicts of interest. This includes understanding whether the SPAC team has existing fiduciary obligations to other entities in the same industry, or perhaps even a pre-existing interest in the target company. Since the underwriters of the SPAC’s listing would already have conducted due diligence on the SPAC’s sponsors and management team, the banks underwriting the acquisition may choose to forgo another round of diligence and only look into the target entity – potentially to the detriment of investors.

While best practices for investigative due diligence are relatively consistent across the industry for IPOs, they are not as well established in the SPAC and de-SPAC market. Balancing the shortened timelines and the different sets of risks that come with SPACs have challenged underwriters to remain nimble and sometimes creative when it comes to determining the scope of diligence.

As the SPAC issuance frenzy becomes a rush to de-SPAC, risks are ramping up and SEC oversight is tightening significantly. Many SPACs will never find a deal, leaving public investors nursing losses. As competition for the right acquisitions heats up, those that do manage to close a transaction risk overpaying or overlooking a major risk in their target’s background. Getting due diligence right from the start can protect both capital and reputations.