In August 2018, President Trump signed a bill expanding the scope and powers of the Committee on Foreign Investment in the United States (CFIUS). The new law has important implications for Chinese investment in the US market and may complicate capital flows between two countries already engaged in a trade war.

What is CFIUS?

CFIUS is a US government committee that advises the American president on whether to block certain foreign investments on national security grounds.

The members of CFIUS include the Secretaries of Treasury, State, Defense, Homeland Security, and others. CFIUS has existed in one form or another since 1975 to review the national security implications of foreign investment in the United States. CFIUS may reject a proposed transaction, such as the foiled USD 1.2 billion merger between the Chinese company Ant Financial and MoneyGram. CFIUS may later approve a restructured version of a rejected deal, as occurred when the Chinese investment firm Creat Group Corporation was able to acquire a German entity after its American operations were excluded from the deal.

There have only been five instances of a US president blocking investments. Significantly, all five of these decisions either stopped investment from Chinese companies or were due to concerns over possible Chinese involvement. President George H.W. Bush canceled the sale of an American aircraft parts manufacturer to a Chinese state-owned enterprise. President Obama prevented two companies that were Chinese owned and operated from deals in the renewable energy and semiconductor sectors. So far, President Trump has also blocked two deals. In September 2017, he barred the USD 1.3 billion purchase of Lattice Semiconductor by Chinese-backed Canyon Bridge Capital Partners. In March 2018, the US president halted the USD 117 billion acquisition of chip manufacturer Qualcomm by the Singaporean entity Broadcom, reportedly because of the potential influence of the Chinese company Huawei.

Yet the impact of a CFIUS review may reach beyond these relatively rare, high-profile cases. There have been hundreds of CFIUS reviews in just the past decade, and even the announcement of a CFIUS investigation can hurt the stock price of a firm involved in the investigation. Under the newly bolstered CFIUS regime, it is plausible that the number of reviews could increase in the years to come.

What is FIRRMA?

On 13 August 2018, President Trump signed into law the Foreign Investment Risk Review Modernization Act (FIRRMA). The new law is the most comprehensive legal update to CFIUS in three decades. It was proposed by both Republican and Democratic senators and overwhelmingly passed both the House of Representatives and Senate.

Under the law, investors connected to foreign governments, such as sovereign wealth funds, must now file notifications for certain planned transactions with US companies. These notifications used to be voluntary. Affected transactions will then undergo a 30-day review process to decide whether a complete CFIUS review is needed.

CFIUS also gained the power to review certain non-controlling foreign investments into US companies. Previously, CFIUS was only permitted to review transactions that resulted in foreign ownership of a US company. Under the new law, CFIUS may review investments that cause the transfer of critical technologies out of the country, or involve critical infrastructure or sensitive personal data. The committee may now also review real estate deals located close to US government property.

Which Industries Will be Impacted by FIRRMA?

The industries that could be impacted by FIRRMA consist primarily, but not exclusively, of sectors that have military applications or implications. Prior to the passing of FIRRMA, the US Department of Homeland Security listed 16 critical infrastructure sectors in the United States, including communications, energy, financial services, and information technology. Similar language describing these critical infrastructure sectors was used in FIRRMA, which is most relevant to businesses dealing with international M&A deals, private equity, and real estate. Two months after FIRRMA became law, the US Treasury released interim CFIUS regulations with a more specific scope of 27 industries, such as those relating to the manufacturing or production of aluminum, computers, semiconductors, aircraft, petrochemicals, guided missiles, and space vehicles.

Time will tell how the new CFIUS oversight will influence foreign investment in cutting-edge tech industries in the United States. Defense Innovation Unit Experimental, a US government entity, released a report on Chinese acquisitions of US tech companies that notes that “China is investing in the critical future technologies that will be foundational both for commercial and military applications: artificial intelligence, robotics, autonomous vehicles, augmented and virtual reality, financial technology and gene editing.” The report also emphasizes that Chinese investments in early stage technologies in the US “are consistent with China’s goals” of tech innovation and industrial development, such as those laid out in the country’s five-year plans and the Made in China 2025 policy.

However, the M&A deals that fall under CFIUS review could potentially extend beyond the above industries. According to one study by professors from Harvard, Princeton, and the University of Chicago, US politicians and government agencies were also more likely to oppose Chinese M&A efforts in industries that were either economically distressed or that were not equally open to investment in China. More generally, around 40% of CFIUS filings have resulted in investigations. With an increase in CFIUS filings after FIRRMA, it remains to be seen how these figures will change.

How Has FIRRMA Been Received in China?

In theory, CFIUS and FIRRMA are directed at any foreign investor. In practice, most analysts agree that the new law is directed at China. China is likely to be affected the most by the new law, partly because of the sheer quantity of Chinese FDI coming into the US and partly because CFIUS regulates the sectors of the US economy that most interest Chinese investors.

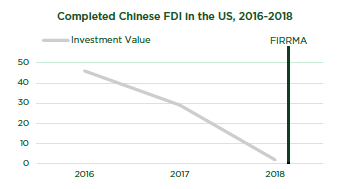

As the graph here shows, Chinese FDI into the US has been decreasing since 2016, even before the passage of FIRRMA. From January to May 2018, Chinese FDI in the US was only USD 1.8 billion, a 92% drop from the same period in 2017. Analysts attribute this decline to both Chinese domestic controls over outbound investments and stricter US regulatory review that predates FIRRMA.

Mainstream Chinese observers predict that FIRRMA will further worsen the policy environment for Chinese investment in the US. However, a few of these analysts say that FIRRMA simply codifies what CFIUS has already been doing for several years, and does not change the actual policy environment all that much. These commentators say that the main effect of the law is psychological: Chinese investors and US companies are likely to give more weight to risk from CFIUS, making the former more cautious about investing in the US and the latter more reluctant to deal with Chinese counterparts.

There are also signs that a regime similar to CFIUS is taking shape in China. China has been tightening domestic review of outbound investment, as well as considering increasing scrutiny of foreign investment in China. In February 2018, China’s state planner added news media, cross-border water resources development and weapons development to its list of “sensitive” sectors for offshore investment while maintaining restrictions on real estate, hotels, motion picture studios, sports clubs, and private equity funds that have no investments in the “real economy.”

In addition, China is attempting to build and implement a more comprehensive system to review foreign investment in China. Currently, China’s Anti-Monopoly Law has a national security review procedure. In 2015, China passed a National Security Law, although the law does not detail how the latest national security reviews would be implemented. Therefore, China’s “CFIUS” counterpart remains in its early stages.

What are the Political Risk Implications?

Globally, more and more countries are putting restrictions on inbound FDI. The UK, Canada, Australia, and others have imposed new controls on foreign investment, a trend that has also been discussed in relation to China. These measures heighten the need for thorough knowledge of political risk, which includes an increasingly complex regulatory environment. Aside from regular pre-investment due diligence, investors increasingly need to be aware of the changing political climates of the countries in which they are operating.

Political risk can stem from regulatory bodies that are impacted by both domestic politics and international tensions. For example, in 2017 CFIUS was understaffed as political appointees – who could have different review styles – were not filling their positions quickly enough. Partly as a result, in the same year CFIUS was generally inclined to “just say no” to Chinese investors instead of working out a mitigation plan. On China’s side, Qualcomm called off its USD 44 billion deal to buy NXP Semiconductors in July 2018 after Chinese anti-trust regulators postponed approval amid the US–China trade war.

Even beyond CFIUS and FIRRMA, investors need to have a keen ear for political sentiment. In 2006, the UAE government-owned Dubai Ports World was unanimously approved by CFIUS to operate several major container terminals in the United States. However, coming only five years after the 9/11 terrorist attacks, the deal provoked the opposition of Democratic and Republican lawmakers, as well as the general public. Congress stepped in to block the acquisition, and Dubai Ports World promptly handed control of the US container terminals to an American entity. In such cases, analysis of the political environment surrounding a possible M&A deal could have helped foresee and respond to these difficulties.

The extent to which FIRRMA will change the regulatory environment is now unknown, but at the very least the new law implies that the US is more concerned about Chinese investment in critical sectors and is likely to make such deals more difficult. This empowered CFIUS oversight and the parallel trade war reveal the complexity and contradictions of international finance. As the global economy continues to become increasingly interconnected, the US and other countries have simultaneously sought to restrict certain investments due to national security. The net effect of these conflicting orientations will play out in the coming years. Meanwhile, it’s clear that investors will need to be comfortable with ambiguity.

Further Reading

Political Risk: How Businesses and Organisations Can Anticipate Global Insecurity, Condoleezza Rice and Amy Zegart, Weidenfeld & Nicolson, 2018, pp. 163–165.