On Sunday, 11 August, Argentines soundly rebuked President Mauricio Macri’s reform agenda in the country’s primary elections, known locally as PASO. Opposition candidate Alberto Fernández, joined by former President and current Senator Cristina Fernández de Kirchner (no relation) as his running mate, came out on top with a 15-point lead. If repeated in Argentina’s general elections on 27 October, this result could usher in a fresh slate of populism that would bring a reversal to Macri’s pro-market policies. A spread of this magnitude was largely unexpected by investors, who had relied on faulty polling data that suggested a toss-up between Mr. Fernández and Macri.

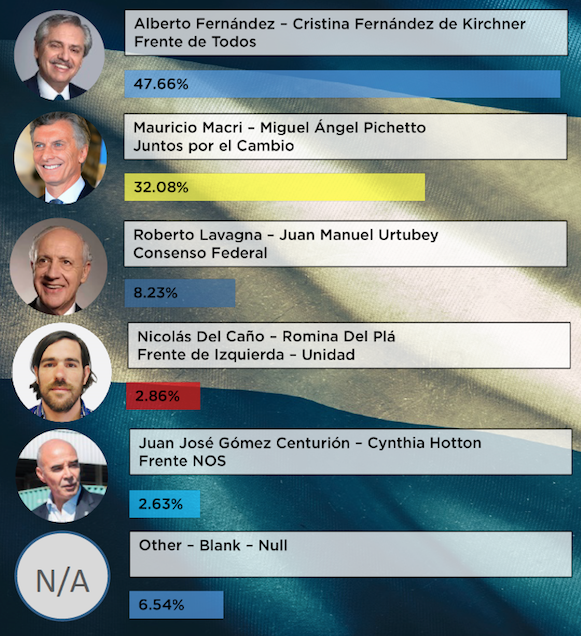

Argentina’s Primary Election (PASO) Results

*Based on a participation rate of 76%. (Source: https://www.resultados2019.gob.ar/)

Why the PASO Results Matter

Since all the presidential candidates ran uncontested within their respective coalitions, the PASO was effectively a rehearsal for the general elections. Participation in the PASO is mandatory for all Argentines over the age of 16, which means that the results could be a harbinger of what is to come. Candidates rely on these results to measure and adjust their campaign strategies. To win the presidency on 27 October, candidates must obtain 45% of the vote, or 40% with a 10-point lead over the runner-up. Failing to do either will trigger a runoff on 24 November.

A Referendum on Macri

Macri’s rise to power was as impressive as it was inopportune. Soon after bringing the country out of a recession in 2016, Macri faced yet another recession last year, brought on by exorbitant interest rate hikes to combat a global run on emerging market currencies. This prompted a USD 57 billion bailout package from the IMF with additional austerity requirements. Despite Macri’s attempts to open up Argentina’s economy, currency devaluations, stubborn inflation, and subdued economic growth have made Argentines feel worse off than before. Mr. Fernández, described as a moderate, has openly called for a reversal to many of the reforms Macri pursued to anchor investor confidence. Short on details, Mr. Fernández has promised to expand subsidies for public utilities, loosen monetary policy, and protect local industry from foreign competition.

What This Means for Argentina’s Business Environment

Investors have reason to be concerned. Pundits are unsure whether a Fernández administration will be characterized by the deal-making pragmatism of Mr. Fernández or a return to the interventionist policies of Kirchner’s administration (2007–15). Kirchner presided over an economy markedly hostile to foreign investment, with capital and price controls, nationalizations, a holdout against sovereign creditors, and a politicization of Argentina’s central bank and statistical data administration, among others. She and her closest advisors have also been implicated in multiple scandals. Kirchner herself is involved in 12 ongoing corruption cases related to bribery, embezzlement, and padded public works contracts – allegations she describes as politically motivated by her opponents.

Despite her track record and indictments, Kirchner still maintains a loyal base of supporters. Her anticipated return to the Casa Rosada will be determined by her shrewd political calculations, one of which is to keep her distance from the campaign trail. As running mate, Kirchner hopes to obtain the critical mass necessary to defeat Macri in October by combining her support base with Mr. Fernández’s anti-incumbent appeal. The strategy appears to be working. For his part, Macri chose Miguel Ángel Pichetto, a former ally of Macri’s political opponents, to be his running mate. Like Mr. Fernández, Macri is aware that the election will likely be decided by the moderate vote.

Investors Can Expect the Following Risks Under a Fernández-Kirchner Administration:

- The election results are set to prolong Argentina’s recession. Soon after the PASO results were released, the S&P Merval Index, Argentina’s most prominent stock market index, plunged 48% in USD terms – the second largest drop since 1950. The peso also lost nearly 18% of its value, which means that inflation – already up 54% year-over-year – is likely to rise further. Although these values will ultimately be set by the power dynamics of a Fernández-Kirchner administration, markets are clear that discontinuity in economic policy and Kirchner’s presence in the Casa Rosada warrant an elevation in country risk on Argentine assets. This adds a new drawback to Argentina’s recovery.

- Argentina’s risk of a default on or restructuring of sovereign debt will increase. Dampened economic growth prospects coupled with Mr. Fernández’s support for reversing controls on spending are likely to increase Argentina’s debt burden. The debt to GDP ratio surged to 86% in 2018, a near 30-point increase from 2017. Mr. Fernández has publicly ruled out defaulting on the IMF package, but has highlighted his intentions to renegotiate the terms of the deal. Argentina has defaulted on its debt payments eight times since the country’s independence in 1816 – the most recent being in 2014 when the Kirchner administration denied payment to holdout creditors. Since the PASO elections, both Fitch and S&P have downgraded Argentina’s sovereign credit rating deeper into junk territory, further jeopardizing future favorable lending programs.

- The election adds a new layer of obstacles to the recent Mercosur-EU trade agreement. Despite the free trade agreement’s approval last June, it still faces the uphill task of being ratified by each Mercosur member’s legislature. Mr. Fernández described the agreement as harmful and underscored his intent to review and reject some of its provisions. His political ties to Argentina’s labor unions will increase these odds. Still, Mr. Fernández can expect substantial pressure to support the deal from Argentina’s provincial governors, who exert significant influence on the federal government, and Brazil, whose government threatened to leave Mercosur if Mr. Fernández or Kirchner attempt to sabotage the agreement.